ECONOMICS

Twenty-Seventeen Was a Great Year for Housing, Expect the Same in 2018

By Peter Norman

2017 was a very remarkable year for new housing construction right across Canada (as predicted in this column one year ago!). In addition to the strongest housing starts performance in a decade, there was also remarkable regional convergence, with every region showing gains (in fact every province except one, Newfoundland and Labrador, advanced in 2017). Some 219,000 units were started in 2017, up 11 per cent from 2016 and some 24,000 units higher than the annual average over the past ten years.

The good news is that that many of the factors fueling this growth will continue to provide a boost to housing demand in 2018. But this year will not be without its challenges.

2017 turned out to be a remarkably strong year for job gains right the way across the country. Over 422,000 net new jobs were created within the year—a 15 year record. The largest gains were found in Quebec, B.C. and Ontario. Alberta also saw significant job gains as part of an important bounce back after a recession that lasted for two years.

Job growth, of course, is critical for housing demand as a new job boosts a household’s income and its consumer confidence to undertake larger investments, such as home buying, upgrades or renovations. Typically, there are lags between a pick-up in job growth and a noticeable boost to housing demand—sometimes thought to be about two years. Thus, notwithstanding the strong housing starts in 2017, the job gains last year are likely setting the stage for stronger housing demand over the next few years — particularly in markets like Quebec and Alberta where the gains were so sharp.

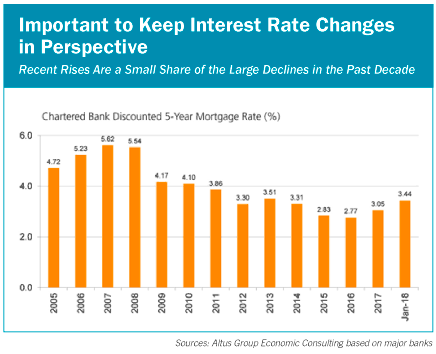

2017 was the year that mortgage interest rates began to retrace some of their long-term trend declines. Many in the industry are concerned that this will pose some sort of risk on the horizon, but the impact that interest rates will have on the 2018 market is likely to be pretty muted. First, while the effective five-year mortgage rate rose about 45 basis points through 2017 and may see some further modest rise in 2018, these changes are still pretty minor in comparison with the almost 300-basis-point decline over the past decade.

In addition, interest rates have more of an impact on housing price than the volume of sales transactions. This is to say that households on the margin of affordability that are ready and willing to buy, will seek lower-priced product rather than withdraw from the market completely. Enough of them across the market means we expect somewhat flatter prices through a period of mild interest rate hikes rather than the sort of frothy pattern seen in recent quarters.

Supply constraints continue to be among the key risks to the housing market. Supply problems, particularly among single-family development land, played a significant role in the turbulence in certain urban markets in the past two years and still threatens to pose problems in 2018. Many urban markets across the country have faced a certain shortage of approved development land, as planning policies coast to coast attempt to densify through restrictive policies.

The most acute examples have been Vancouver and Toronto over the past two years that each had price peak events and periods of turbulence related to supply shortages. But other markets such as Calgary and Regina also continue to have underlying problems with adequate single-family approvals, albeit somewhat masked by the recent recessions in those markets. In general, 2018 is expected to be a strong year for housing demand based on income, employment and migration growth—expect to see more frothy conditions emerge in our most supply-constrained urban markets.

On net we expect housing starts nationally to stay relatively buoyant at about 210,000 units.

Residential renovation activity will also be fueled by many of the same factors such as employment and income growth. Expect about 4 per cent growth in renovation expenditure in 2018, with continued focus on energy efficiency projects but with emerging trends toward home automation and multi-generational adaptations.

Peter Norman is VP & Chief Economist at Altus Group, and leads a national team of economic advisors providing policy analysis, feasibility assessment, and economic intelligence to the home building and real estate industry. He can be reached at peter.norman@altusgroup.com.

External Links: Associations & Governments. Builders & Renovators . Manufacturers & Suppliers

Home . About Us . Subscribe . Advertise . Editorial Outline . Contact Us . Current Issue . Back Issues . Jon Eakes

© Copyright - Work-4 Projects Ltd.